The Fed’s foot is on the gas but the economy is losing altitude

Investors have gone all-in on the bet that the Fed and its central banking colleagues abroad will be successful in turning around a slowing global economy. The melt-up in the S&P since early last month is like Wall Street’s version of pushing your chips to the middle of the table. It’s not really surprising seeing that in October the Fed, the Bank of Japan, the European Central Bank and the People’s Bank of China all expanded their balance sheets for the first time in more than two years, giving the markets a massive shot of adrenaline.

As far as actual economic results, there aren’t many green shoots to be found around the world. Last week the U.S. reported unimpressive Industrial Production and Retail Sales numbers, dragging the Atlanta Fed’s widely watched U.S. GDP tracking model down to just a 0.4% pace for the current quarter. See https://bit.ly/2r3ifvH. China also had poor production and sales results. Japan’s economy is growing at only 0.2% and Germany just barely avoided recession with a 0.1% growth rate. Not an encouraging picture.

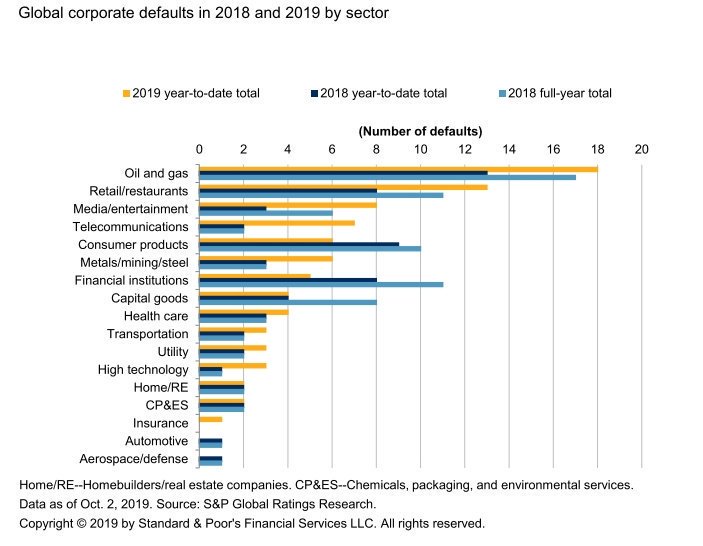

Given all the monetary firepower that the central banks have deployed over the past decade, they don’t have much to show for it. But the thing that sticks out to us, and the real threat to the global economy is pictured in the chart below. Despite the appearance of policy success as reflected by rising equity prices, corporate bond defaults are actually increasing. If the policy was working, that wouldn’t be happening.

We have written extensively on the danger that a deteriorating credit sector poses for policymakers. (See Time to BBBe Careful). Recently the IMF raised a red flag on the state of U.S. corporate risk-taking and declining leveraged loan quality. See https://bit.ly/35m9DPL. They ominously predict that in the event of an economic downturn “corporate debt at risk of default would rise to $19 trillion, or nearly 40 percent of the total debt in eight major economies.” Yes, that’s trillion with a ‘T’. The IMF also noted that “surges in financial risk-taking usually precede economic downturns.”

To say that this is potentially a massive problem is the understatement of the year. The market, in this case the corporate bond market, has officially become the economy. An explosion in global debt pushed by extreme central bank policies since the 2008 recession is a burden that steals from future growth, meaning that a simple economic slowdown carries not just cyclical but systemic risks of default. It is the Fed’s greatest nightmare. And they can’t allow it to happen.

Rather than seeing the Fed’s actions for what they are, an act of disaster prevention for the credit markets, many investors are taking the dynamic of falling rates as a cue to pile into riskier trades. There’s an unshakable faith that the Fed will allow no harm to come to them. It seems like a misreading of macro conditions to us, and an unwise strategy after a 10 year-long bull run, but for now the market obviously disagrees.

It’s gotten so crazy that even one of the world’s largest mutual fund companies is urging baby-boomers to lay off the stocks. According to Fidelity Investments, more than one-third of boomers (born 1944-1964, and entering retirement) have a greater than 70% allocation to equities, and one-in-ten were invested entirely in stocks. See https://bloom.bg/2pxjvXu. This has disaster written all over it when the market eventually turns.

We’ve long said that some enormous trading opportunities will present themselves at that point when the markets lose faith in the Fed and realize that current policies will fail to stop the rot. We’re not there yet, but it’s getting close. In the meantime take the market rally as a gift to raise cash, and stay long the front end rate complex.

One thought on “Stall Speed”