The Trader’s Perspective is written from a trader’s perspective of risk versus reward. The goal is to simplify the process of macroeconomic analysis and look for opportunities beyond consensus opinion.

The Trader’s Perspective is written from a trader’s perspective of risk versus reward. The goal is to simplify the process of macroeconomic analysis and look for opportunities beyond consensus opinion.

Written June 21, 2020

In “The L-Shaped Recovery“, we predicted that a combination of demand destruction, job market uncertainty, rising debt, and a shift in consumer behavior would hinder the economy from achieving a rapid recovery from the COVID pandemic.

Since that writing, the Fed has taken the unprecedented step of intervening directly in support of the credit markets, producing a spectacular V-shaped rebound in the financial markets. But as we all know, the market is not the economy.

The economic template that the current public health crisis is most often compared to is the Great Depression of the 1930s, but a more instructive precedent for what the future holds might be that of Japan, which is still trying to shake off the effects of the financial market bubble that popped in 1989.

To put the excesses of 1980s Japan in context, it was said that the 280 acres of land within the walls of the Imperial Palace in central Tokyo was worth more than the entire state of California. At the time, this became the benchmark against which all other insane real estate and lending valuations were linked. When it inevitably crashed, Japan, Inc. tried borrowing their way out of trouble. More than 30 years later, and after racking up an eye-watering debt-to-GDP ratio of 279%, they’re still trying to find a way out.

In Japan, bankruptcy is not seen as a financial tool deployed to clear the decks of bad debt but rather as a cultural stain, one of humiliation and loss of face. So corporate Japan, and the country itself, stumbles onward like a zombie, burdened by mountains of legacy debt, unable to reap the benefits of innovation that leaner balance sheets would enable. This interminable trap is so ubiquitous that it even has its own name: Japanification.

Unfortunately, the Fed is headed down a similar path. Not only by backstopping the credit markets but by actively pushing prices higher, the Fed has allowed almost every corporation access to cheap money. It may be necessary, but just like the never-ending policy of quantitative easing destroyed the price discovery function in the equity markets, the unintended consequence of credit intervention is doing the same to the bond market. Normally where good corporate governance is rewarded and bad decisions are punished, everybody now gets a trophy.

In my day job as an editor for a financial news service, I spend a large portion of my time reading press releases from companies tapping into an almost unlimited supply of liquidity in the credit markets, with most of it going to refinance revolving bank debt incurred during the pandemic. Borrowing is literally exploding.

While this widespread refi effort is tactically beneficial in the near term to bridge the gap in cash flow created by the virus lockdown, the long term risk is that it will allow bad capacity to remain on the books, keeping unproductive companies alive and leaving little room for innovation and for fresh entities to thrive.

Corporate America was already running record levels of debt and leverage before the pandemic hit. Half of the investment-grade bond market is precariously rated BBB, just one notch above junk. Wide-scale bankruptcies and credit downgrades are indeed a systemic threat in a weakened economy, and it is forcing the Fed’s hand to prevent the entire system from snowballing downhill and out of control. But, like Japan, the unintended consequence of today’s policies will be a debt burden that will take years, if not decades, to climb out from under.

In a note to clients last week, Bridgewater Associates’ Ray Dalio warned of a “lost decade” for the equity markets as profit margins get squeezed by debt servicing costs. See here https://bloom.bg/3hMBVtC.

We tend to agree and would use this recent rebound in financial markets to reduce risk exposure while sticking with core long positions in the US dollar, short-term treasuries, and gold.

Written May 24, 2020

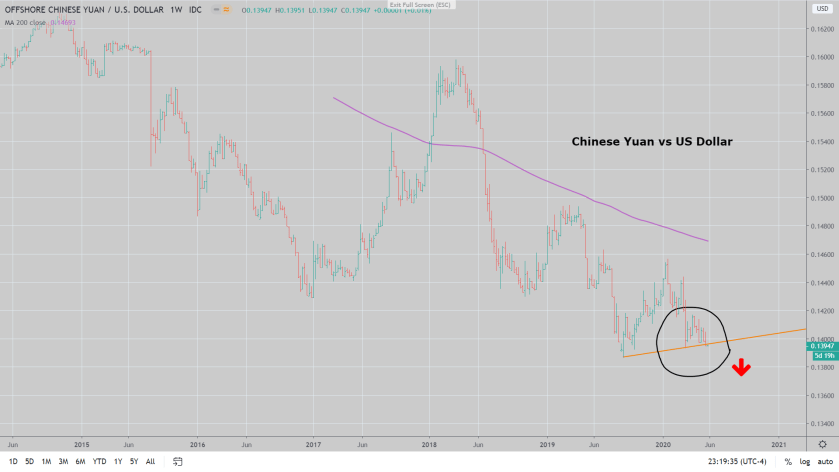

The Chinese yuan finished last week near its lowest level in more than a decade as investors began to bet with their feet, heading for the exits over concern that the country is compounding its economic problems with geopolitical moves that are already generating widespread condemnation and even greater uncertainty.

The post-pandemic economic landscape presents a test for the regime that has long prided itself in delivering on an unspoken bargain where one-party rule is tolerated in exchange for consistent economic growth.

However, a sure tell that the government’s grip is slipping was its failure to set an economic growth target for the upcoming year during last week’s National People’s Congress, the annual planning meeting of the Chinese Communist Party. It might seem like an insignificant detail, but for the first time since it began providing GDP estimates in 1990 the central body declined to be bound by a projection that it may not be able to meet. It is a big deal, and the obvious conclusion is that the economy on the mainland is worse than it outwardly appears.

China’s recalcitrance in dealing with COVID-19 has also turned global public opinion against it. As a result, doing business with the Chinese in the future is going to come under much more scrutiny than in the past.

Despite the allure of 1.4 billion potential consumers, it now won’t be so easy to turn a blind eye to the tilted playing field China has erected to their advantage, as much of the world has done since China’s inclusion into the World Trade Organization in 2001.

The U.S. Senate took the first step last week by passing a bill by a 100-0 margin requiring Chinese firms to adhere to American accounting standards or risk being delisted from our exchanges, also a big deal. Other measures will follow.

The pandemic exposed many countries’ over-reliance on Chinese manufacturing and is forcing most to reconsider basing their supply chains elsewhere. Japan even earmarked part of its economic stimulus fund specifically to help its manufacturers shift production out of China.

The bottom line is, the rules of international trade are being rewritten and China is not going to like the changes.

Further complicating matters, China is lashing out at the west’s insistence on an investigation into the origins and handling of the virus. Within the space of a few weeks they’ve made moves to block certain Australian exports, threatened to cut off the supply of critical pharmaceutical ingredients to the U.S., and imposed their own national security laws on Hong Kong. So much for the idea of “one country, two systems” that was the founding principle agreed to by both parties when the British turned Hong Kong over to China in 1997 and that has allowed the former colony to thrive as an international financial center.

Not content to stop there, the Chinese navy is scheduled to begin live-fire military exercises later this month as part of an amphibious assault training operation on an island controlled by Taiwan. As the Wall St. Journal asked in a May 21 op-ed titled “China Moves on Hong Kong”, is Taiwan next?

At the risk of stating the obvious, political isolation from global trading partners can only be seen as a negative for the economy.

Plan A for Chinese authorities to counteract these economic headwinds is with traditional fiscal and monetary stimulus, along with a heavy dose of infrastructure spending. But the effectiveness of that approach is questionable as the country is already swimming in overcapacity, and debt. It’s the demand side of the equation that is lacking.

Plan B would be a devaluation of the currency, which the market is beginning to sniff out. In theory, this would spur demand by making Chinese-produced goods more competitively priced. In reality, it would propel the dollar higher, unleashing a deflationary wave on a world already under enormous pressure from falling prices.

The Fed and other central banks have done an impressive job of rescuing the credit and equity markets from the depths of the pandemic panic in March, but a Chinese devaluation would slam the lid on any hopes of reflating the global economy.

Our core portfolio positions remain long of the US dollar, front-end treasuries, and gold.

Written May 10, 2020

Last week, for the first time in the country’s history, the financial markets began discounting the possibility of negative interest rate policy.

On Thursday, the December Fed Funds futures contract settled above par (100.00), implying that traders have moved beyond talking in the abstract about negative interest rates and started betting with real money that the Federal Reserve will be forced by events into crossing a line they’ve long insisted they would not step over.

Japan, Europe, Switzerland, Sweden, and Denmark currently have negative interest rates, policy legacies left over from fighting the last recession in 2008. The theory was that people would be so repulsed by having to pay a bank to hold their money that they would gladly spend it instead, stimulating the economy in the process. It hasn’t exactly worked out that way.

Rather than driving consumer demand, negative interest rates have resulted in a minefield of unintended consequences. Besides the lack of confidence it conveys to the public on behalf of impotent policymakers, it has clogged the banking system and perverted the lending process.

Count us among those who previously thought there was little chance that the Fed would follow the rate policies of its Japanese and European counterparts. But as we recently wrote in “The L-Shaped Recovery“, the pandemic has exposed and accelerated the threat of debt deflation that could end up triggering waves of bankruptcies.

The deflationary scenario was brought into stark relief after we recently came across a chart overlaying the Economic Cycle Research Institute’s Weekly Leading Index (WLI) with the US consumer price index (see below). As the name suggests, the WLI anticipates economic activity 2 to 3 quarters in the future. If the correlation with the CPI holds, it means prices could begin dropping later this summer.

Just as the value of debt falls in real terms in an inflationary environment, it rises in deflationary times. The problem is compounded by declining cash flows as a result of weak economic activity, making it harder to service that debt and potentially creating a serious problem for highly leveraged economies like ours.

The other moving part in the relationship between debt and deflation is the U.S. dollar. If the Fed’s policy rate is anchored at zero and market yields can’t keep pace with falling prices for goods and services, real yields (the nominal yield minus the rate of inflation) will rise, driving the dollar higher and depressing the price of imports domestically and commodities globally. As we said in “The Biggest Trade in the World“, “the risk to the broader economy is that a stronger dollar triggers a doom loop of debt deflation, where slower global growth causes the dollar to rise and a stronger dollar, in turn, depresses prices and causes growth to slow.”

As has been the case with every rate cut in this cycle, the market will lead the way for the Fed’s next move. And given the risk that rising real yields could pose to the prospects for a recovery, investors are concluding that the Fed may have no choice but to take rates negative.

Besides being long-time proponents of the U.S. dollar and front-end treasuries as core investment themes, we recently recommended adding a position in physical gold. Gold may be subject to bouts of selling if the dollar continues to rise, as many traders still reflexively see the two as inversely correlated. But because there doesn’t seem to be any limit on central bank money printing, gold will shine as the ultimate store of value in a world of increasingly negative interest rates.

Written April 27th, 2020

Successful traders are always asking themselves two questions in the course of analyzing markets: 1) given a set of known inputs, are markets behaving as expected? and 2) if not, why not?

Since the COVID-19 pandemic crashed the world’s financial markets last month, central banks have responded with extraordinary measures to stabilize markets and prop up their respective economies.

For its part, the Fed has undertaken policies on a scale unprecedented in the history of finance, radically expanding their balance sheet and going so far as lending directly to municipalities and buying junk bond ETFs in the open market. Essentially printing money, but on steroids.

The equity markets have responded favorably, much as one would expect given the deluge of liquidity. It’s a reflexive response conditioned by a decade of the Fed propping up asset prices every time the markets stumbled. Will it last? Nobody knows.

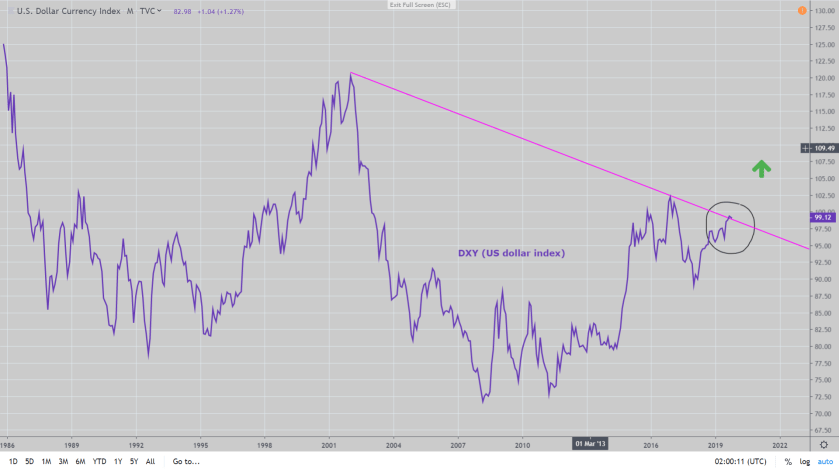

However, the part of this scenario that is not going according to plan is potentially the most consequential for the financial markets. The US dollar needs to weaken. Big time. For a global economy staring at a tsunami of deflation, it is the most critical element to achieving a durable reflation of commodities and equity prices and restoring confidence in many regions of the world, especially the emerging markets.

This is not lost on central bank officials. In fact, if you were asked to come up with a policy to destroy your own currency, moves by the Fed and the Treasury over the past month to explode the federal deficit would be it.

The speculative trading community initially took the cue. According to CFTC data, the specs began shorting the dollar in the middle of March as rates went to zero and the money printing presses began working overtime.

But since then, not only hasn’t the dollar gone down, it is higher instead.

The latest study by the Bank for International Settlements estimates the world’s short position in the dollar at about $13 trillion, much of it based on dollar debt held by offshore banks and corporations, representing the largest aggregate position in the financial markets by far.

Currency swap facilities instituted and expanded by the Federal Reserve with the intention of ensuring these entities access to dollar funding helped settle the markets late last month, but the currency’s appreciation since then is a sure sign that it won’t be enough. For many of these foreign corporations, swap lines are of little value if their respective central banks don’t have sufficient reserves to swap or US Treasury securities to pledge as collateral.

Also, printing trillions won’t do much good if there is no turnover, or velocity, of that money due to the collapse in business activity. It just ends up in the vaults of institutions that don’t need it, crowding out the weaker borrowers.

Against all expectations, the steady grind higher in the dollar in recent weeks is a red flag that this massive short trade is about to get squeezed.

The implications will be felt everywhere. The risk to the broader economy is that a stronger dollar triggers a doom loop of debt deflation, where slower global growth causes the dollar to rise and a stronger dollar, in turn, depresses prices and causes growth to slow.

As we’ve been recommending for more than a year, stick with long positions in the dollar and front-end treasuries. In our last piece “The L-Shaped Recovery“, we suggested adding physical gold and taking advantage of near-term strength in equities to reduce exposure. If the dollar starts to accelerate, things could get ugly. Quickly. And despite the Fed’s insistence on not taking interest rates negative, it’s not impossible that this will end up being their next move.

Investors blindsided by the virus shouldn’t compound their problems by thinking that things will immediately return to normal once it passes.

It’s hard to predict the outcome of unprecedented events because, by definition, they’ve never happened before and handicapping them is nearly impossible. The models used by scientists to justify a complete shutdown of the global economy to mitigate the spread of the coronavirus may turn out to be off by a factor of ten, or more. It’s not meant as an indictment of them but an acknowledgment that like most investors trying to navigate the markets, they haven’t done this before either. At least not on this scale.

For that same reason, we should be skeptical of forecasts of a swift rebound once the virus passes. Just like how faulty data skews computer models, those calls seem to grossly underestimate the potential long-term damage to consumer confidence, supply chains, and the rejection of globalism in general. Garbage in, garbage out.

We were warning all of last year that markets were in an increasingly precarious position. See “Stall Speed“, “Tipping Point” and “Powell Plays for Time“. A decade of excessive monetary stimulus provided by the major central banks since the last recession in 2009 had all but destroyed the price discovery function of markets and dulled investors to signs of trouble. Record equity prices as a result of the Fed’s guiding hand and abundant liquidity obscured unsustainable debt burdens, slowing economic growth, declining corporate earnings and deteriorating credit quality. Many believed, and likely still do, in the Fed’s ability to extend the business cycle forever and revive the 11-year old bull market. To us the contradiction is nuts but as the old saying goes, the markets can stay irrational longer than you can stay solvent.

The virus exposed some serious vulnerabilities of the global economy, most notably the level of debt. As a result, we think that the economic adjustment to new societal norms and changes in consumption behaviors will take longer to play out than most of us can conceive.

Government officials and other commentators who are pushing a narrative of a V-shaped economic recovery are wrong on two basic assumptions.

1) It ignores the global debt dynamic, and the possibility that this event represented a tipping point long in the making. An unintended consequence of quantitative easing programs was companies taking advantage of cheap money to buy back their own stock and pay dividends rather than investing in their businesses. That’s now over, especially for any entity accepting federal assistance. And it should be.

Despite low rates and lots of government cash on offer, corporations will be forced to de-leverage their balance sheets to align with a new economic reality, which will come at the expense of capital spending, investment, and employment. Borrowing and refinancing costs could also rise as many companies suffer rating downgrades or find access to funds restricted by wary lenders. Businesses operating on thin margins, even large corporations, may not survive. If they do they are likely to run mean and lean for years to come rather than re-staff their employee ranks.

2) The claim of pent-up demand is ludicrous. Consumers are in shock. If you weren’t worried about your job before, you sure as hell are now. Just because your job might have survived the initial wave of layoffs it doesn’t mean it won’t get eliminated as the fallout ripples through the economy. Free government handouts will keep the lights on but don’t fool yourself into thinking that it is stimulative.

Rent payments that got waived in April are going to have to be paid in full in May or June, in addition to the current amount due. Credit card interest will continue to accrue. Most mortgages have been securitized, making it impossible to extend the terms and simply add missed payments onto the back end of the loan. Sure, you can defer several months’ payments but the bank is going to want all that back in a lump sum sometime this summer. And if you skipped eating out ten times or missed three haircuts while on lockdown, you’re not going to then go order ten meals when the curfew is lifted.

To steal a term from former Secretary of Defense Donald Rumsfeld, there are still too many unknown unknowns right now. To conclude that things will return to pre-virus normal is fantasy.

Many of us grew up hearing stories about the Great Depression of the 1930s. Unemployment then peaked at around 25%, and it affected spending habits for two generations. People hoarded, they saved. Like my parents and their parents before them, they never let go of that mindset.

Governments and central banks are literally throwing money at both the markets and at citizens alike in an effort to stop the bleeding, but for the reasons stated above it may not be enough. Don’t confuse liquidity with solvency. The Fed might be able to address the former, but for many, the latter is still very much a risk.

One big positive for the economy is the resilience of the American consumer. The labor force is more flexible, means of communication and transportation more efficient and capital markets more dynamic than it was last century. Technology helps society to adapt to changing conditions almost instantaneously. In large measures, people can now work and shop from home. The shutdown may actually open our eyes to better and more efficient ways of conducting our day-to-day lives.

While nobody could have forecast the COVID-19 virus, at this time last year we recommended being long of the U.S. dollar and front-end treasuries as a play on slowing global growth. We still like those positions but would urge readers to consider adding physical gold to their portfolios and use this rebound in stocks to reduce risk exposure. In the months and years ahead, many countries will be making moves to weaken their currencies (i.e. printing money) to stimulate their economies and regain an advantage in international trade. Gold is the flip-side of the depreciating fiat money coin.

So when William Devane appears on your TV urging you to buy precious metals as a hedge against “unstable governments printing paper money”, know that he may be on to something.

Investors have gone all-in on the bet that the Fed and its central banking colleagues abroad will be successful in turning around a slowing global economy. The melt-up in the S&P since early last month is like Wall Street’s version of pushing your chips to the middle of the table. It’s not really surprising seeing that in October the Fed, the Bank of Japan, the European Central Bank and the People’s Bank of China all expanded their balance sheets for the first time in more than two years, giving the markets a massive shot of adrenaline.

As far as actual economic results, there aren’t many green shoots to be found around the world. Last week the U.S. reported unimpressive Industrial Production and Retail Sales numbers, dragging the Atlanta Fed’s widely watched U.S. GDP tracking model down to just a 0.4% pace for the current quarter. See https://bit.ly/2r3ifvH. China also had poor production and sales results. Japan’s economy is growing at only 0.2% and Germany just barely avoided recession with a 0.1% growth rate. Not an encouraging picture.

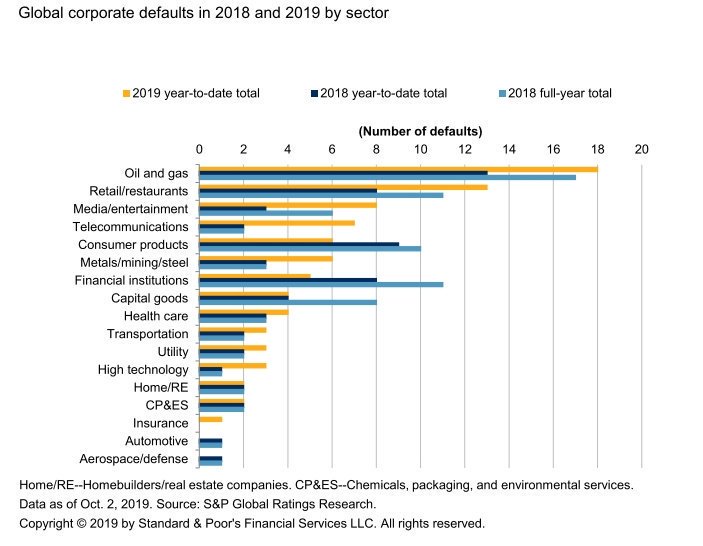

Given all the monetary firepower that the central banks have deployed over the past decade, they don’t have much to show for it. But the thing that sticks out to us, and the real threat to the global economy is pictured in the chart below. Despite the appearance of policy success as reflected by rising equity prices, corporate bond defaults are actually increasing. If the policy was working, that wouldn’t be happening.

We have written extensively on the danger that a deteriorating credit sector poses for policymakers. (See Time to BBBe Careful). Recently the IMF raised a red flag on the state of U.S. corporate risk-taking and declining leveraged loan quality. See https://bit.ly/35m9DPL. They ominously predict that in the event of an economic downturn “corporate debt at risk of default would rise to $19 trillion, or nearly 40 percent of the total debt in eight major economies.” Yes, that’s trillion with a ‘T’. The IMF also noted that “surges in financial risk-taking usually precede economic downturns.”

To say that this is potentially a massive problem is the understatement of the year. The market, in this case the corporate bond market, has officially become the economy. An explosion in global debt pushed by extreme central bank policies since the 2008 recession is a burden that steals from future growth, meaning that a simple economic slowdown carries not just cyclical but systemic risks of default. It is the Fed’s greatest nightmare. And they can’t allow it to happen.

Rather than seeing the Fed’s actions for what they are, an act of disaster prevention for the credit markets, many investors are taking the dynamic of falling rates as a cue to pile into riskier trades. There’s an unshakable faith that the Fed will allow no harm to come to them. It seems like a misreading of macro conditions to us, and an unwise strategy after a 10 year-long bull run, but for now the market obviously disagrees.

It’s gotten so crazy that even one of the world’s largest mutual fund companies is urging baby-boomers to lay off the stocks. According to Fidelity Investments, more than one-third of boomers (born 1944-1964, and entering retirement) have a greater than 70% allocation to equities, and one-in-ten were invested entirely in stocks. See https://bloom.bg/2pxjvXu. This has disaster written all over it when the market eventually turns.

We’ve long said that some enormous trading opportunities will present themselves at that point when the markets lose faith in the Fed and realize that current policies will fail to stop the rot. We’re not there yet, but it’s getting close. In the meantime take the market rally as a gift to raise cash, and stay long the front end rate complex.

In the weeks since our last comment the major central banks, led by the Fed, have ridden in hard to try and extend the life of what is already the oldest economic expansion in history. A confluence of declining corporate earnings forecasts, weakening industrial and retail activity, and persistent funding shortfalls in dollar-based securities markets has forced the Fed to administer CPR on the financial system. Despite the outwardly calm appearance, the Fed is very nervous, literally throwing money at both the economy and the markets in an effort to prevent a downturn in global growth from metastasizing into another financial crisis. Massive levels of debt and leverage encouraged by profligate central bank policies over the past decade now mean that the normal cycles of the economy…and the inevitable periods of weakness…cannot be allowed to play out naturally without risking a complete meltdown in the financial markets. (See BBBe Careful).

In October alone the Fed restarted their balance sheet expansion, ramped the daily overnight repo financing allocation and cut rates for the third time in four months. It’s a veritable fire hose of liquidity that pumps between $60 and $100 billion per month into the marketplace. It’s also a dead giveaway that everything is not fine. Former Dallas Fed advisor Danielle DiMartino-Booth aptly described the state of play as the Fed trying to “suppress the unknown, that at its best is credit volatility and at its worst systemic risk.”

So far the deluge of liquidity, at least initially, seems to be having the desired effect. Like every other time in the last eleven years that the Fed has fired up another round of quantitative easing, regardless of prevailing economic trends, record highs in the S&P were all but certain to follow. This time is no different. And almost as if the third consecutive quarterly decline in year-on-year corporate earnings don’t matter. The title of our recent piece ‘Liquidity Trumps Fundamentals‘ speaks for itself.

Don’t be fooled by Jay Powell’s attempt at downplaying the need for future rate cuts and reassuring investors that the expansion still has legs. See https://on.wsj.com/2pTHtfE Having to hit the panic button after nearly a decade of policy stimulus is definitely not a position in which anyone on the board of governors thought they would find themselves. It’s becoming abundantly clear that without a major reset in asset prices and a restructuring of the role of the central banks in the markets, rates will never be normalized. The Fed is headed into a policy cul-de-sac from which there is no exit. Like an addict, they’ve hooked the markets on easy money. Make no mistake, the minute stocks stumble, rate cuts will be back on the table. As much as they’d like everyone to believe it, this is no simple mid-cycle policy adjustment. It’s a one way street toward zero interest rates. If there’s a lesson from the past year, it’s that the economy remains vulnerable and that the bull market in equities and credit is not self-sustaining without the Fed’s foot firmly on the gas.

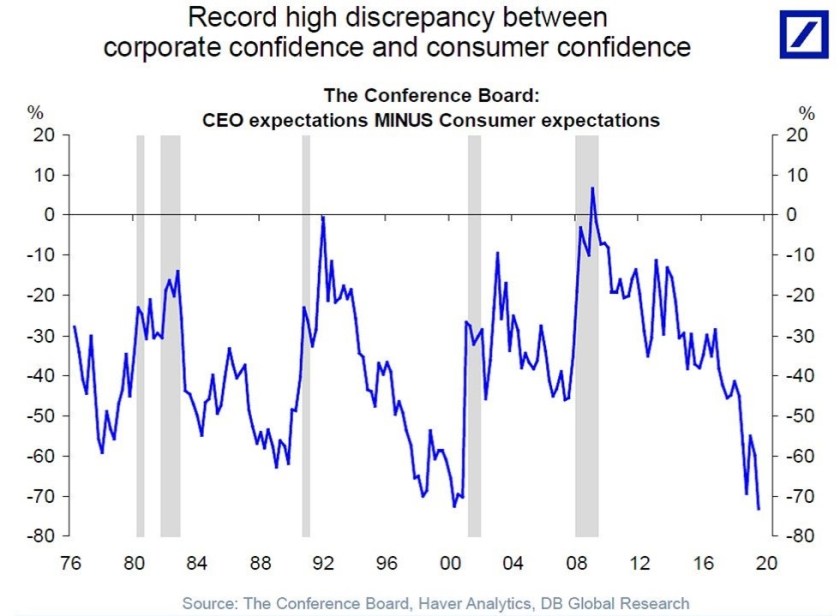

Presumably, corporate CEOs get this. These are the guys making decisions on hiring and capital investment. The latest survey of CEO confidence is shockingly bad and contrasts starkly with optimism among consumers (see charts below). Visually, the surveys are very similar to the chart that became popular several months ago comparing opposing trends in equities and bond yields. Coined with the name “Jaws” it illustrated two major financial benchmarks projecting distinctly different economic outcomes. (See “Jaws” Could Take a Bite Out of Markets). Which indicator is ultimately proven right (bonds or stocks) remains an open question. The two charts below from The Conference Board on confidence reveals a similar contradiction. History shows two things: 1) CEO confidence leads consumer confidence and 2) a sharp deterioration in CEO confidence has immediately preceded each of the last five recessions (the gray shaded areas). But as with the original Jaws chart, which side is ultimately right and how these normally correlated, but currently divergent, trends snap back into line is yet unknown.

Our preference is to bet on the side of history. The heavy dose of hopium from coordinated central bank intervention driving stocks and bond yields higher in the past few weeks will fade in time. It’s another sugar high. We have been long the front end U.S. rate complex for all of 2019 and still see this sector as the most effective play on slowing global growth. The Fed has a trigger finger with respect to cutting rates. Be patient, but the widespread position flush underway in the bond market this week is an excellent opportunity to reload those long positions between now and year-end.

Or, expressed another way:

Written October 2, 2019

Yesterday’s sharp deterioration in risk sentiment is a sign that the equity market and its patrons at the Fed may have a couple of serious problems: 1) The latest numbers from the Institute for Supply Management (ISM) suggests the US economy may be close to, or already in recession and 2) the Fed has been too slow to recognize it. Neither of these issues is exactly new news but the stock market’s seemingly oblivious reaction to the growing danger has been nothing short of remarkable. Until now.

The continued erosion of benchmark ISM survey data on U.S. manufacturing, its worst reading since 2009, was punctuated by a complete collapse in the forward-looking new export orders component. See https://bloom.bg/2oWfXgK. The disruption in commerce and global supply chains from trade wars is real and intensifying. Similarly, contractionary readings on factory production from China and Europe this week only added to the recessionary drumbeat.

It is undeniable that the Fed underestimated the deceleration in the economy. Their hesitancy to ease when signs of economic weakness first appeared earlier this year probably means that a recession is now inevitable. They missed the boat. Even if the Fed cut rates aggressively now it may not matter. And that possibility is starting to occur to investors who had come to rely on the Fed as a consistent backstop for asset prices.

It feels like the markets are at a tipping point. The major central banks have spent a decade throwing trillions at the economy and have little to show for it except for unprecedented levels of income inequality. But it hasn’t stopped them from pressing forward with more of the same policies. The renewed race to the bottom on interest rates is becoming less effective while at the same time increasingly desperate.

The failed WeWork IPO might have rung the proverbial bell in this era of easy money and stretched valuations. Fundamentals matter. Earnings, which they clearly don’t have, matter. Like Pets.com, the poster child of absurdity from an earlier bubble, WeWork will go down as an example of “what were they thinking?” for years to come. See https://bit.ly/2nE1y8N.

As I noted in my two previous pieces (see VIX Cheap as Impeachment Threat Grows and Liquidity Trumps Fundamentals), the most obvious trades in this shifting paradigm are to be long volatility and long the front-end rate market. Historically, October is more volatile than most other months. And the lurch lower in key economic data points could be the catalyst that makes volatility in equities, bonds, and FX all suddenly appear to be ridiculously underpriced.

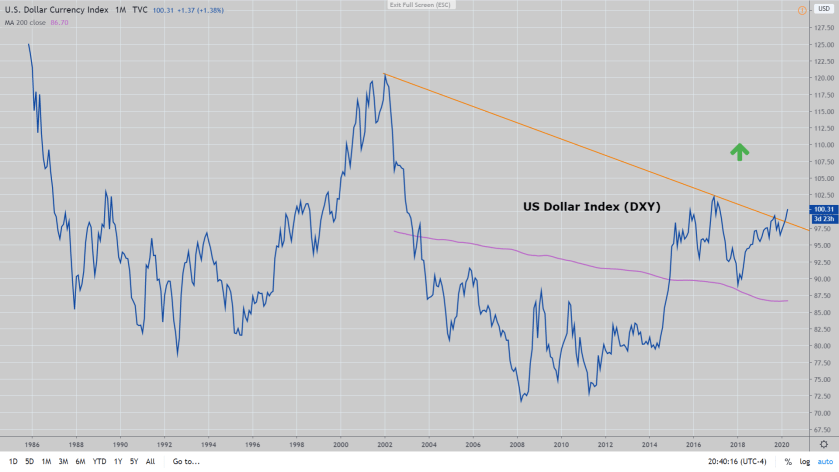

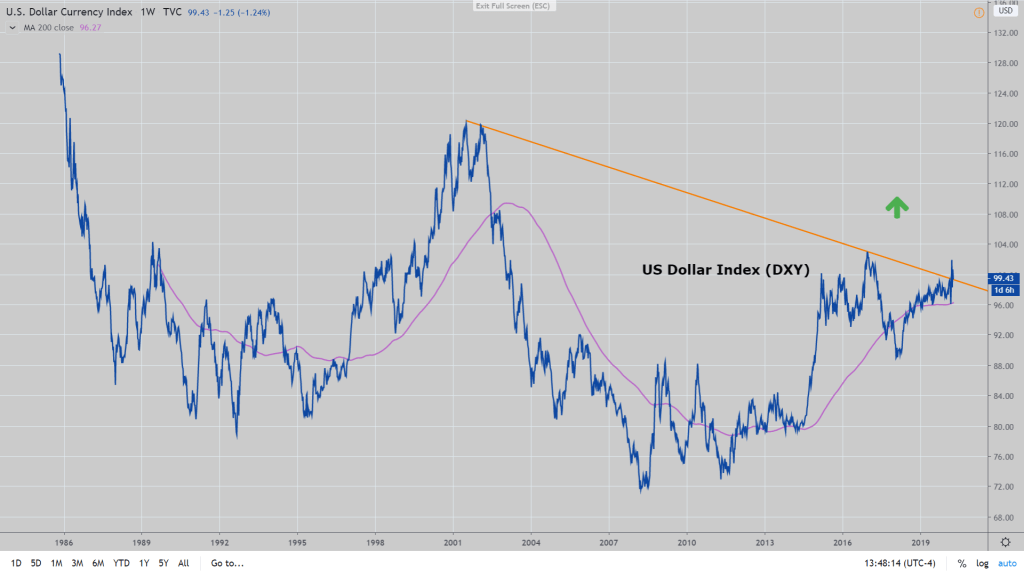

Furthermore, anyone who doubts that the Fed could take rates back to zero, and quickly, has not looked at the U.S. dollar. The growing global dollar shortage, which we’ve written about extensively, is pushing the buck up through multi-decade resistance (see Fed Rate Cut: Too Little, Too Late). The long term dollar index (DXY) chart is very bullish, and if the USD gets legs it will make the 2018 emerging market selloff look tame by comparison. The Fed can’t afford for that to happen and will be forced to keep cutting rates to try to prevent it.

Written September 26, 2019

Just like the equity market’s general complacency over the uncertainty created by a potential presidential impeachment, it is exhibiting a similar lack of interest in the ongoing liquidity squeeze in short-term funding markets.

A sharp spike in overnight financing rates last week due to a scarcity of bank reserves was initially dismissed as an unexpected confluence of technical factors. Everything from quarterly tax bills, treasury auction settlements, and principal and interest payments were blamed for draining an unusual amount of money from the system and causing an acute shortage of free reserves. Overnight rates were said to have traded as high as 10% before the Fed was forced to step in with emergency funds. The panic passed but the underlying problem hasn’t gone away. Lots of confusion still hangs over the money markets. Financing remains tight, enough so that the Fed has had to supplement the system with cash every day since. This is not normal and the longer it goes on the explanation that it is merely a temporary quirk becomes less credible.

As of now, the consensus opinion is that this problem will fix itself simply by a turn of the calendar past quarter-end (September 30). That seems to be a big leap of faith. In a Bloomberg piece today former Minneapolis Fed President Narayana Kocherlakota says that regulatory changes after the 2008 crisis, like more stringent capital and leverage requirements, have restricted the amount of free reserves in the financial system and banks’ willingness to lend those reserves among themselves. See https://bloom.bg/2mGcO3B. None of this was a problem while the Fed was expanding its balance sheet and providing almost limitless liquidity. Only when the Fed began to shrink its balance sheet a year ago did this unintended consequence emerge.

The explosion in the issuance of US dollar-based debt, both domestic and foreign, during the previous decade of easy money policies created a massive need to finance that debt. What has now become obvious is that without additional liquidity provided by the Fed, there just aren’t enough dollars in the system to go around. Kocherlakota notes that “the financial system is acting like it has $1.3 billion in excess reserves rather than the actual $1.3 trillion.”

This means the Fed can forget about any plans they might have had for normalizing interest rates and reducing their balance sheet. Quite the opposite, it slants the probabilities in the direction of even lower rates. The problem in the money markets is structural and has disrupted one of the financial markets’ most essential functions. Until they figure out how to fix it, simple liquidity will become an ever-important consideration for investors. Fundamental investment strategies don’t matter much if they can’t be financed.

The fourth quarter of 2019 will see two issues elevated that were not big considerations in the current quarter: domestic political uncertainty and liquidity uncertainty. These factors should lead to a general increase in market volatility as well as heightened concern over funding availability. This will almost certainly force banks and asset managers to begin paring back positions for year-end earlier than ever. Additionally, rate cuts at Fed meetings in October (Oct 29-30) and December (Dec 10-11) will be in play as the Fed seeks to offset the slowing economy and keep funding pressures contained.

The two simplest trade opportunities are 1) long equity volatility such as the VIX (see VIX Cheap as Impeachment Threat Grows) and 2) long Eurodollar interest rate futures, such as the Dec 2021 contract. Policy rates in the U.S. are on their way to zero and there’s a lot left in this trade.

Written September 24, 2019

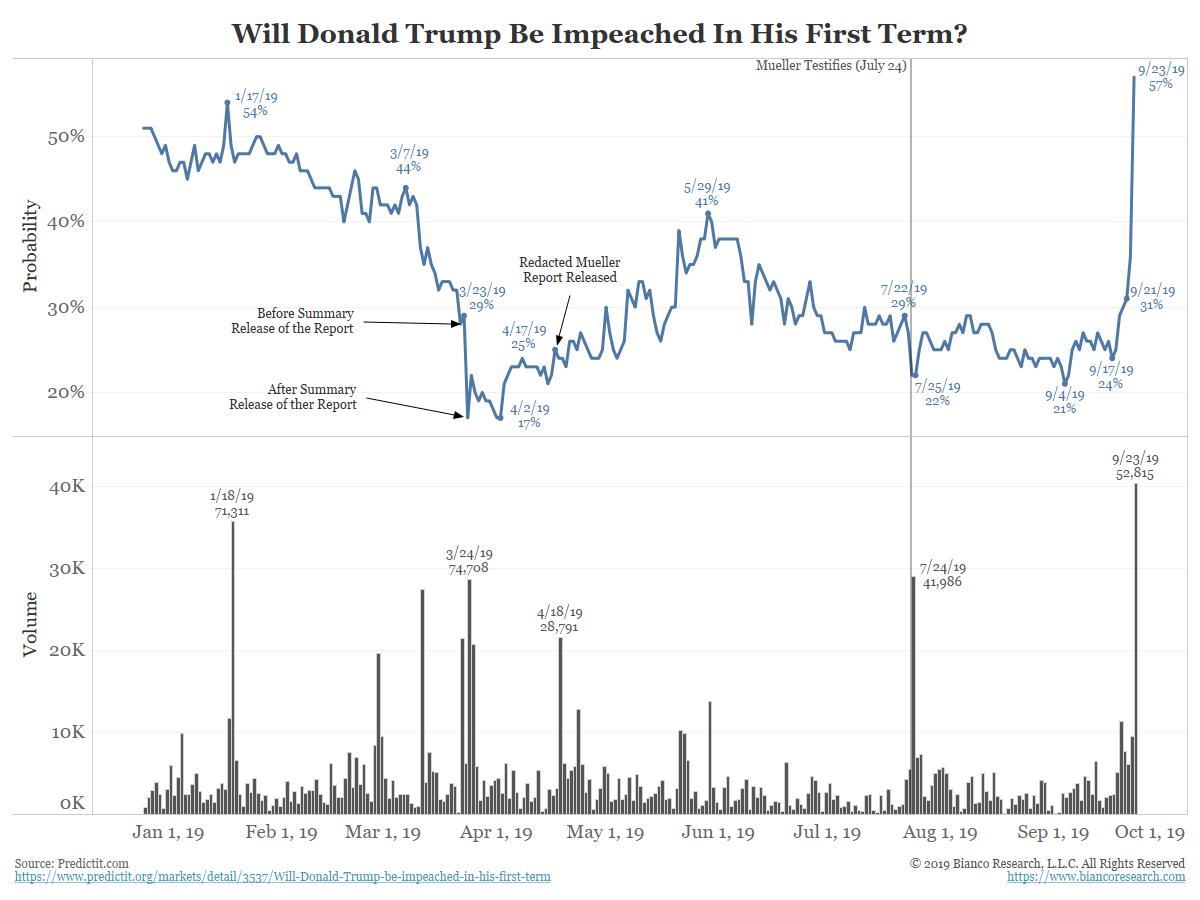

Despite a lack of facts, Washington has been consumed by accusations that President Trump acted improperly in a phone call with his Ukrainian counterpart, with many claiming that it qualifies as an impeachable offense. That conclusion may or may not be true. More will be known after acting Director of National Intelligence Joseph Maguire addresses the whistleblower complaint that sparked the controversy before the House Intelligence Committee on Thursday, September 26.

Odds for Trump’s impeachment spiked yesterday on the betting market Predictit to 57%, the highest level this year. This matches a growing number within the Democrat caucus that believe the president should be removed.

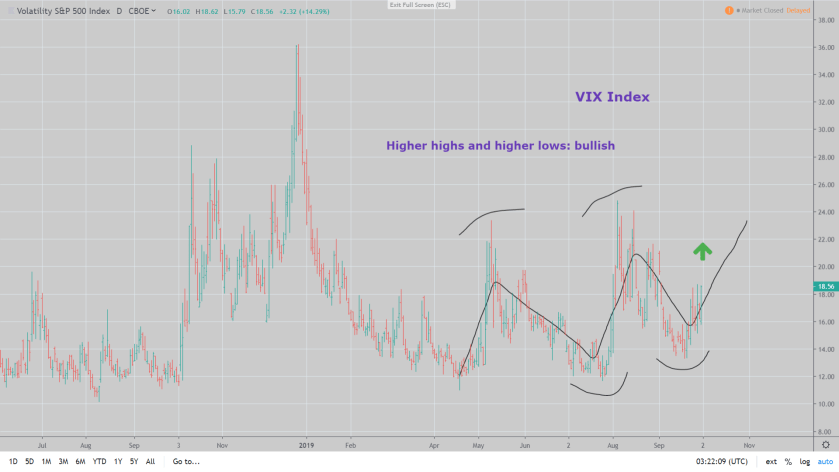

At the same time, the S&P is trading about 1% from record highs and the broad market’s primary fear gauge, the CBOE Volatility Index (VIX Index), is near the lower end of its range. In short, a picture of complacency.

It’s hard to see how these two conditions are mutually compatible for very long. One side is wrong.

The hallmark of the Trump presidency has been a bull market in stocks, and any threat to his tenure would almost certainly inject a level of uncertainty that would be reflected through lower prices. While it is unknown if he will be impeached, that outcome and any potential negative fallout in the equity markets presents the more favorable risk/reward trading profile. The bet is that the markets are currently underpricing the disruption and volatility that such an event would produce.

Even though the VIX appears subdued, price action is positive. Since spring, the VIX has been tracing out a classically bullish pattern of higher highs and higher lows (see chart below). As long as each prior low print holds, in this case, the September 19 low of 13.30, pullbacks are buying opportunities.