Debt deflation starts the U.S. on a path to negative interest rates

Written May 10, 2020

Last week, for the first time in the country’s history, the financial markets began discounting the possibility of negative interest rate policy.

On Thursday, the December Fed Funds futures contract settled above par (100.00), implying that traders have moved beyond talking in the abstract about negative interest rates and started betting with real money that the Federal Reserve will be forced by events into crossing a line they’ve long insisted they would not step over.

Japan, Europe, Switzerland, Sweden, and Denmark currently have negative interest rates, policy legacies left over from fighting the last recession in 2008. The theory was that people would be so repulsed by having to pay a bank to hold their money that they would gladly spend it instead, stimulating the economy in the process. It hasn’t exactly worked out that way.

Rather than driving consumer demand, negative interest rates have resulted in a minefield of unintended consequences. Besides the lack of confidence it conveys to the public on behalf of impotent policymakers, it has clogged the banking system and perverted the lending process.

Count us among those who previously thought there was little chance that the Fed would follow the rate policies of its Japanese and European counterparts. But as we recently wrote in “The L-Shaped Recovery“, the pandemic has exposed and accelerated the threat of debt deflation that could end up triggering waves of bankruptcies.

The deflationary scenario was brought into stark relief after we recently came across a chart overlaying the Economic Cycle Research Institute’s Weekly Leading Index (WLI) with the US consumer price index (see below). As the name suggests, the WLI anticipates economic activity 2 to 3 quarters in the future. If the correlation with the CPI holds, it means prices could begin dropping later this summer.

Just as the value of debt falls in real terms in an inflationary environment, it rises in deflationary times. The problem is compounded by declining cash flows as a result of weak economic activity, making it harder to service that debt and potentially creating a serious problem for highly leveraged economies like ours.

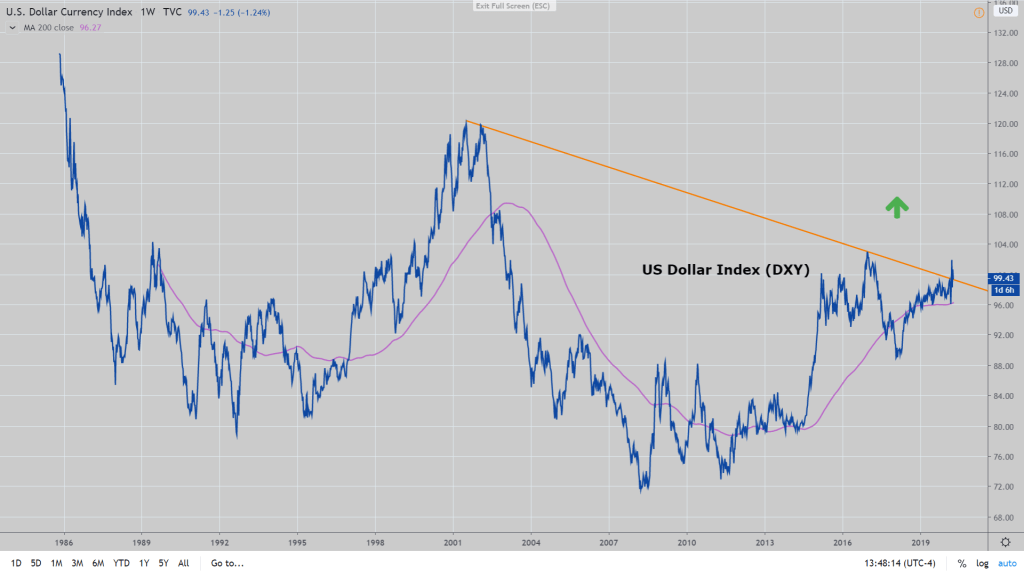

The other moving part in the relationship between debt and deflation is the U.S. dollar. If the Fed’s policy rate is anchored at zero and market yields can’t keep pace with falling prices for goods and services, real yields (the nominal yield minus the rate of inflation) will rise, driving the dollar higher and depressing the price of imports domestically and commodities globally. As we said in “The Biggest Trade in the World“, “the risk to the broader economy is that a stronger dollar triggers a doom loop of debt deflation, where slower global growth causes the dollar to rise and a stronger dollar, in turn, depresses prices and causes growth to slow.”

As has been the case with every rate cut in this cycle, the market will lead the way for the Fed’s next move. And given the risk that rising real yields could pose to the prospects for a recovery, investors are concluding that the Fed may have no choice but to take rates negative.

Besides being long-time proponents of the U.S. dollar and front-end treasuries as core investment themes, we recently recommended adding a position in physical gold. Gold may be subject to bouts of selling if the dollar continues to rise, as many traders still reflexively see the two as inversely correlated. But because there doesn’t seem to be any limit on central bank money printing, gold will shine as the ultimate store of value in a world of increasingly negative interest rates.