Declining economic growth may become too much for equity markets to ignore

Written October 2, 2019

Yesterday’s sharp deterioration in risk sentiment is a sign that the equity market and its patrons at the Fed may have a couple of serious problems: 1) The latest numbers from the Institute for Supply Management (ISM) suggests the US economy may be close to, or already in recession and 2) the Fed has been too slow to recognize it. Neither of these issues is exactly new news but the stock market’s seemingly oblivious reaction to the growing danger has been nothing short of remarkable. Until now.

The continued erosion of benchmark ISM survey data on U.S. manufacturing, its worst reading since 2009, was punctuated by a complete collapse in the forward-looking new export orders component. See https://bloom.bg/2oWfXgK. The disruption in commerce and global supply chains from trade wars is real and intensifying. Similarly, contractionary readings on factory production from China and Europe this week only added to the recessionary drumbeat.

It is undeniable that the Fed underestimated the deceleration in the economy. Their hesitancy to ease when signs of economic weakness first appeared earlier this year probably means that a recession is now inevitable. They missed the boat. Even if the Fed cut rates aggressively now it may not matter. And that possibility is starting to occur to investors who had come to rely on the Fed as a consistent backstop for asset prices.

It feels like the markets are at a tipping point. The major central banks have spent a decade throwing trillions at the economy and have little to show for it except for unprecedented levels of income inequality. But it hasn’t stopped them from pressing forward with more of the same policies. The renewed race to the bottom on interest rates is becoming less effective while at the same time increasingly desperate.

The failed WeWork IPO might have rung the proverbial bell in this era of easy money and stretched valuations. Fundamentals matter. Earnings, which they clearly don’t have, matter. Like Pets.com, the poster child of absurdity from an earlier bubble, WeWork will go down as an example of “what were they thinking?” for years to come. See https://bit.ly/2nE1y8N.

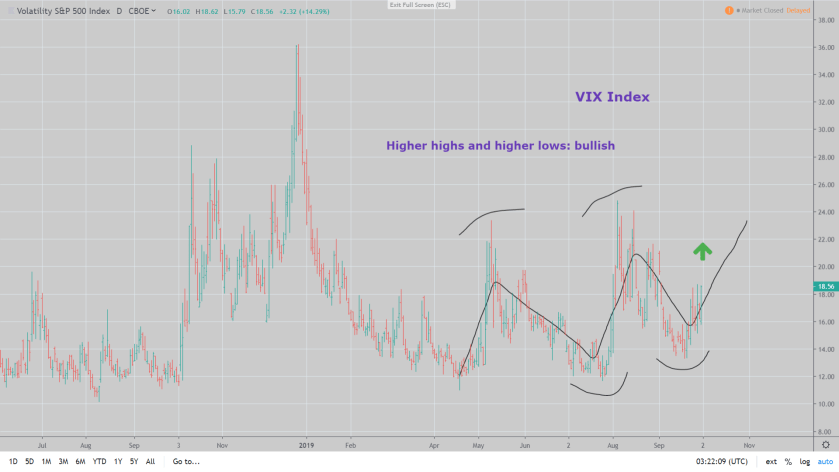

As I noted in my two previous pieces (see VIX Cheap as Impeachment Threat Grows and Liquidity Trumps Fundamentals), the most obvious trades in this shifting paradigm are to be long volatility and long the front-end rate market. Historically, October is more volatile than most other months. And the lurch lower in key economic data points could be the catalyst that makes volatility in equities, bonds, and FX all suddenly appear to be ridiculously underpriced.

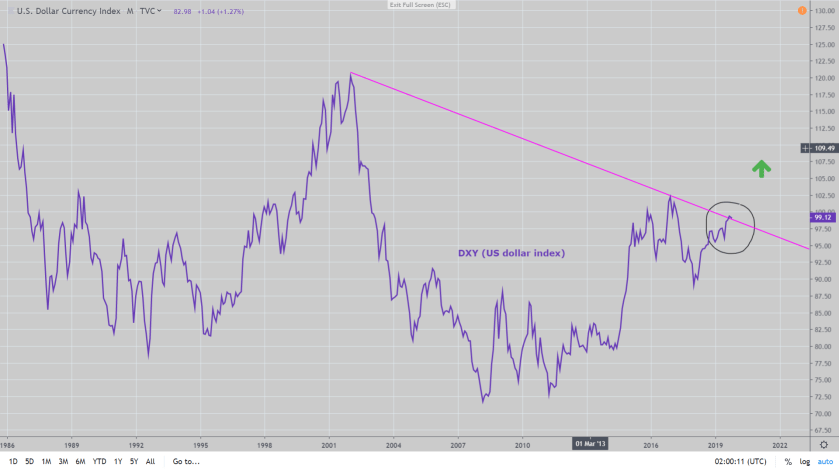

Furthermore, anyone who doubts that the Fed could take rates back to zero, and quickly, has not looked at the U.S. dollar. The growing global dollar shortage, which we’ve written about extensively, is pushing the buck up through multi-decade resistance (see Fed Rate Cut: Too Little, Too Late). The long term dollar index (DXY) chart is very bullish, and if the USD gets legs it will make the 2018 emerging market selloff look tame by comparison. The Fed can’t afford for that to happen and will be forced to keep cutting rates to try to prevent it.