Diverging paths of the economy and the market continues to be a study in contradictions

In the weeks since our last comment the major central banks, led by the Fed, have ridden in hard to try and extend the life of what is already the oldest economic expansion in history. A confluence of declining corporate earnings forecasts, weakening industrial and retail activity, and persistent funding shortfalls in dollar-based securities markets has forced the Fed to administer CPR on the financial system. Despite the outwardly calm appearance, the Fed is very nervous, literally throwing money at both the economy and the markets in an effort to prevent a downturn in global growth from metastasizing into another financial crisis. Massive levels of debt and leverage encouraged by profligate central bank policies over the past decade now mean that the normal cycles of the economy…and the inevitable periods of weakness…cannot be allowed to play out naturally without risking a complete meltdown in the financial markets. (See BBBe Careful).

In October alone the Fed restarted their balance sheet expansion, ramped the daily overnight repo financing allocation and cut rates for the third time in four months. It’s a veritable fire hose of liquidity that pumps between $60 and $100 billion per month into the marketplace. It’s also a dead giveaway that everything is not fine. Former Dallas Fed advisor Danielle DiMartino-Booth aptly described the state of play as the Fed trying to “suppress the unknown, that at its best is credit volatility and at its worst systemic risk.”

So far the deluge of liquidity, at least initially, seems to be having the desired effect. Like every other time in the last eleven years that the Fed has fired up another round of quantitative easing, regardless of prevailing economic trends, record highs in the S&P were all but certain to follow. This time is no different. And almost as if the third consecutive quarterly decline in year-on-year corporate earnings don’t matter. The title of our recent piece ‘Liquidity Trumps Fundamentals‘ speaks for itself.

Don’t be fooled by Jay Powell’s attempt at downplaying the need for future rate cuts and reassuring investors that the expansion still has legs. See https://on.wsj.com/2pTHtfE Having to hit the panic button after nearly a decade of policy stimulus is definitely not a position in which anyone on the board of governors thought they would find themselves. It’s becoming abundantly clear that without a major reset in asset prices and a restructuring of the role of the central banks in the markets, rates will never be normalized. The Fed is headed into a policy cul-de-sac from which there is no exit. Like an addict, they’ve hooked the markets on easy money. Make no mistake, the minute stocks stumble, rate cuts will be back on the table. As much as they’d like everyone to believe it, this is no simple mid-cycle policy adjustment. It’s a one way street toward zero interest rates. If there’s a lesson from the past year, it’s that the economy remains vulnerable and that the bull market in equities and credit is not self-sustaining without the Fed’s foot firmly on the gas.

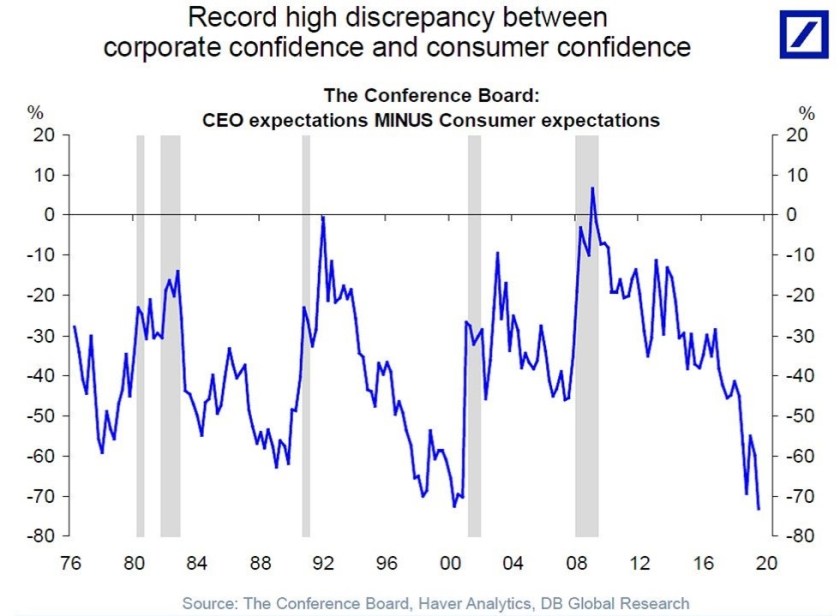

Presumably, corporate CEOs get this. These are the guys making decisions on hiring and capital investment. The latest survey of CEO confidence is shockingly bad and contrasts starkly with optimism among consumers (see charts below). Visually, the surveys are very similar to the chart that became popular several months ago comparing opposing trends in equities and bond yields. Coined with the name “Jaws” it illustrated two major financial benchmarks projecting distinctly different economic outcomes. (See “Jaws” Could Take a Bite Out of Markets). Which indicator is ultimately proven right (bonds or stocks) remains an open question. The two charts below from The Conference Board on confidence reveals a similar contradiction. History shows two things: 1) CEO confidence leads consumer confidence and 2) a sharp deterioration in CEO confidence has immediately preceded each of the last five recessions (the gray shaded areas). But as with the original Jaws chart, which side is ultimately right and how these normally correlated, but currently divergent, trends snap back into line is yet unknown.

Our preference is to bet on the side of history. The heavy dose of hopium from coordinated central bank intervention driving stocks and bond yields higher in the past few weeks will fade in time. It’s another sugar high. We have been long the front end U.S. rate complex for all of 2019 and still see this sector as the most effective play on slowing global growth. The Fed has a trigger finger with respect to cutting rates. Be patient, but the widespread position flush underway in the bond market this week is an excellent opportunity to reload those long positions between now and year-end.

Or, expressed another way: